NET ASSET VALUE, DIVIDEND DECLARATION, 2023 DIVIDEND TARGET AND PORTFOLIO AND FINANCE UPDATE

The board of Directors (the “Board“) of Impact Healthcare REIT plc (ticker: IHR), the real estate investment trust which gives investors exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, is pleased to provide the following business and trading update for the quarter to 31 December 2022.

NET ASSET VALUE

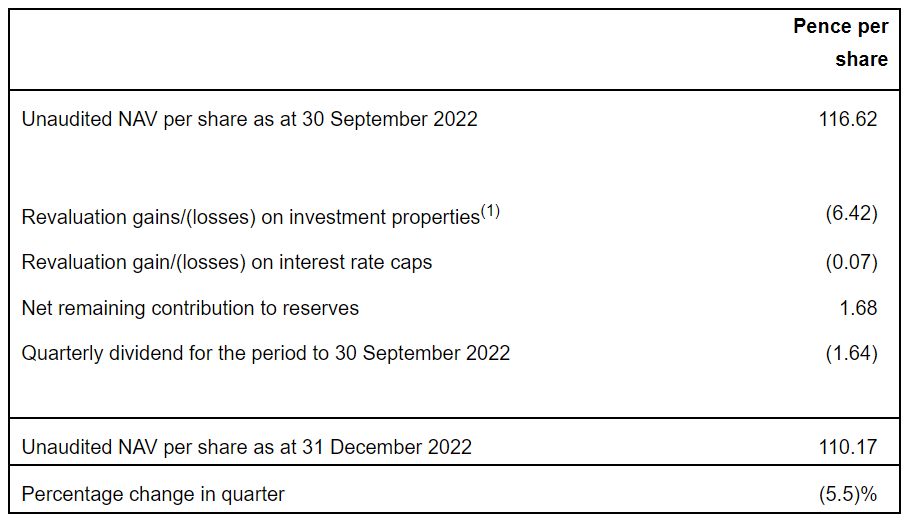

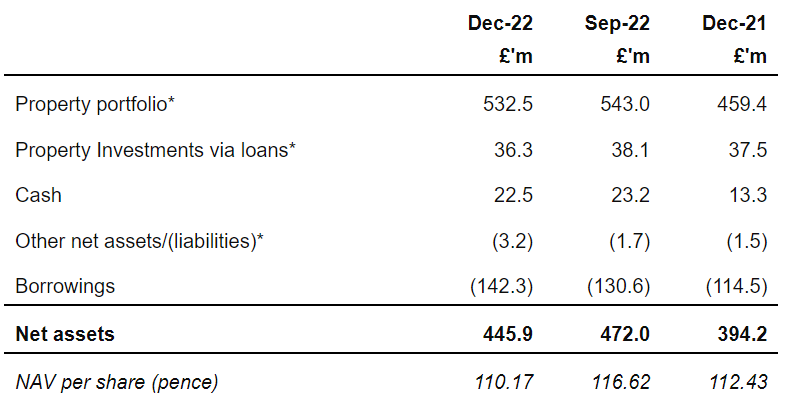

- Unaudited net asset value (“NAV”) as at 31 December 2022 was £445.9 million, 110.17 pence per share. This represents a reduction of 5.5%, or £26.1 million (6.45 pence per share), against the 30 September 2022 NAV of £472.0 million (116.62 pence per share).

- The investment portfolio has been independently valued by the Group’s external valuer Cushman & Wakefield. The Group’s EPRA “topped up” Net Initial Yield at 31 December 2022 is 6.98%, an upward movement of 30 basis points over the quarter as a result of changes in yields across the real estate sector driven, in large part, by increases in interest rates during 2022.

- The NAV attributable to the ordinary shares of the Company is calculated under International Financial Reporting Standards (“IFRS“) and incorporates the independent portfolio valuation at 31 December 2022 and net income for the period. EPRA NTA as at 31 December 2022 was 110.08 pence per share (30 September 2022: 116.46 pence per share) and excludes the fair value of derivatives.

UNAUDITED TOTAL ACCOUNTING RETURN, DIVIDEND DECLARATION AND 2023 DIVIDEND TARGET

- The unaudited NAV total return for the year was 3.77%, comprising dividends paid in the year of 6.508 pence per share and a 2.26 pence per share reduction in NAV.

- The Board remains confident in our underlying strategy and that the business model will continue to deliver attractive returns to investors.

- The Board has today declared the Company’s fourth interim dividend for the year ended 31 December 2022 of 1.635 pence per ordinary share, payable on 24 February 2023 to shareholders on the register on 10 February 2023. The ex-dividend date will be 9 February 2023. This dividend will be paid as a Property Income Distribution (“PID”). This delivers on the Company’s annual dividend target of 6.54 pence per share for the year ended 31 December 2022.

- The Company continues to deliver a fully cash covered dividend from both unaudited EPRA and Adjusted Earnings per share, with dividend cover of 128% and 108% from EPRA and Adjusted Earnings, respectively, in the year to 31 December 2022(2).

- In line with the Company’s progressive dividend policy, under which it seeks to grow its target dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year, the target dividend for the year to 31 December 2023 will increase by 3.53% to 6.77 pence per share(3). The annualised average uplift was 4.1%, of which, 3.53% has been received in cash in the year.

PROPERTY VALUATION

- The Group’s property portfolio (“Portfolio”) was independently valued at £532.5 million as at 31 December 2022 (valuation as at 30 September 2022: £543.0 million). This represents a 4.0% or £21.6 million decrease in value on a like-for-like basis in the quarter and a net decrease of 1.9% over the quarter including the acquisition of two homes and a disposal. The key movements included:

- 16 rent reviews completed in the quarter at an average uplift of 4% per annum in line with the rental increase cap on these leases, contributing an extra £0.2 million to contracted rent.

- The like-for-like movement in value was primarily driven by the shift in market yields partially offset by the increased rent from the 16 rent reviews outlined above. The EPRA ‘topped up’ net initial yield moved out 30 basis points to 6.98% as at 31 December 2022 (30 September 2022: 6.68%) and reflects the independent valuation of our portfolio with the outward movement reflecting a sector wide change in yields.

- In addition, a further £1.0 million was invested in the quarter on asset management activity, primarily on the refurbishment at Fairview with our operator Welford.

- £13.6 million related to the acquisition of two care homes in the southeast with Belmont healthcare.

- The sale of Attlee, a 68-bed care home in Wakefield, for £2.65 million, which was 4% above its 30 June 2022 book value. As part of our active portfolio management strategy, we are looking at opportunities to dispose of some further care homes which are classified as non-core.

- In addition, our investment in a portfolio of 12 care homes operated by Holmes group, which we invested in by way of a loan, was independently valued at £36.3 million (30 September 2022: £38.1 million) a 4.7% reduction of £1.8 million, similarly reflecting the upward shift in valuations across the sector.

PORTFOLIO UPDATE

- Rent cover across our Portfolio remains strong and was just over 1.8x on average for the 12 months to 30 September 2022, and 1.9x for the quarter to the end of September 2022. Tenants’ detailed operational performance reporting for the quarter to December will be received in February 2023.

- Occupancy at 30 December 2022 was 86.6%, down 0.7% on 30 September 2022 (87.3%), but in line with expected seasonal fluctuations over the Christmas and New Year holiday period. Occupancy has started to recover in January 2023.

- Contracted rent remained flat at £43.1 million(4) at the year-end (at 30 September 2022: £43.2 million) with the increase from 16 rent reviews offsetting the lost rent from the disposal of one care home. Following the year-end, with the investment in the six care homes in January 2023, contracted rent has risen to £47.0 million.

- At 31 December 2022, the Portfolio comprised 135 healthcare properties(5), of which 133 are care homes managed by 13 tenants(6) either by way of a loan with an option to purchase and lease on our standard terms (12 homes), or on fixed-term leases of 20 to 35 years (no break clauses), subject to annual upward-only Retail Price Index-linked rent reviews (with a floor and cap at 2% p.a. and 4% p.a., respectively on 99 leases, and 1% p.a. and 5% p.a. on nine). In addition, the Group owns two healthcare facilities leased to the NHS with an annual CPI uplift. In total, the Group had 14 tenants(6) across its Portfolio.

- Weighted average unexpired lease term across the Portfolio of 19.7 years as at 31 December 2022.

- The Group charges rent quarterly or monthly in advance and has received 100% of rent payments due for the quarter to 31 December 2022. For the quarter to 31 March 2023, the Group has currently received 97% of rent due, including 1% from rent deposits. The overdue rent (£0.4 million) is owed by a single tenant, with whom the Investment Manager is in active discussions regarding rental payments.

FINANCING

- The Group’s gross loan to value (“LTV”) ratio was 23.9% as at 31 December 2022 (30 September 2022: 21.4%) following the drawdown of £10 million under its existing revolving credit facilities. The Group has maintained a healthy level of cash reserves, which stood at £22.5 million at the quarter end.

- In the quarter, the Group increased its revolving credit facility (“RCF”) with HSBC to £75 million and increased its RCF with Virgin Money from £25 million to £50 million and extended the maturity to 2029. The Group also cancelled the £15 million RCF with Metro. The Group has increased the available debt from £206 million to £241 million and the weighted average term of debt from 6.2 years to 6.9 years, with lower margins over SONIA.

- Shortly after the year end, the Group completed on an investment in six care homes for £56 million and drew a further £45 million from banking facilities (with the balance paid for through a share issue). As a result, the Group’s drawn debt increased to £187 million with a gross LTV of 28.7%7. The Group secured a further £50 million interest rate cap at a cost of £1.5 million, which caps SONIA at 3.0% for two years.. The Group has now hedged the interest rates on 80% (£150 million) of drawn debt. The current average cost of drawn debt, including hedging and fixed rate borrowings, is 3.86%.

Summary balance sheet (unaudited)

* Properties within the portfolio and Property Investments via loans are stated at the market value provided by the external valuer and excludes the IFRS effects of guaranteed rent reviews and initial lease rental payments.

Notes:

(1) Includes investment in properties directly and by way of loans.

(2) Based on weighted average shares for the year. This does not take into consideration the incremental shares issued on 11 January 2023.

(3) This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

(4) Contracted rent includes all post tax income from investment in properties, whether generated from rental income or post tax interest income.

(5) Includes exchanged and under construction assets.

(6) Belmont, Careport, Carlton Hall, Electus Healthcare, Holmes Care, Maria Mallaband Countrywide Group, Minster and Croftwood (both subsidiaries of Minster Care Group), NHS Cumbria, Optima, Prestige, Renaissance, Silverline and Welford.

(7) Current debt drawn, divided by Gross Assets as at 31 December 2022 plus acquisitions at cost completed since 31 December 2022.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Andrew Cowley

Mahesh Patel

David Yaldron

Jefferies International Limited

Tom Yeadon, tyeadon@jefferies.com

Neil Winward, nwinward@jefferies.com

Tel: +4420 7029 8000

Winterflood Securities Limited

Neil Langford, neil.langford@winterflood.com

Joe Winkley, joe.winkley@winterflood.com

Tel: +4420 3100 0000

H/Advisors Maitland (Communications Adviser)

James Benjamin, impacthealth-maitland@maitland.co.uk

Alistair de Kare-Silver

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

NOTES:

Impact Healthcare REIT plc acquires, renovates, extends and redevelops high quality healthcare real estate assets in the UK and lets these assets on long-term full repairing and insuring leases to high-quality established healthcare operators which offer good quality care, under leases which provide the Company with attractive levels of rent cover.

The Company aims to provide shareholders with an attractive sustainable return, principally in the form of quarterly income distributions and with the potential for capital and income growth, through exposure to a diversified and resilient portfolio of UK healthcare real estate assets, in particular care homes for the elderly.

The Company has a progressive dividend policy with a target to grow its annual aggregate dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year.

On this basis, the target total dividend for the year ending 31 December 2023 is 6.77 pence per share(3), a 3.53% increase over the 6.54 pence in dividends paid or declared per ordinary share for the year ended 31 December 2022.

The Group’s Ordinary Shares were admitted to trading on the main market of the London Stock Exchange, premium segment, on 8 February 2019. The Company is a constituent of the FTSE EPRA/NAREIT index.