The board of Directors of Impact Healthcare REIT plc (ticker: IHR) (the “Board”), the real estate investment trust which provides investors with exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, today announces its intention to issue new equity in order to acquire an identified pipeline of care homes.

The Company will raise new equity through a placing (the “Placing”) of New Ordinary Shares under the Company’s existing Placing Programme as detailed in the prospectus published by the Company on 27 January 2022 and supplemented by a supplementary prospectus dated 30 March 2022 (together the “Prospectus”). In addition, the Company is proposing to raise up to the Sterling equivalent of €8 million pursuant to an offer for subscription (the “Offer for Subscription” and together with the Placing, the “Issue”).

Highlights

- An issue of New Ordinary Shares at 117.0 pence per New Ordinary Share (the “Issue Price”)

- The Issue Price represents a discount of 4.6 per cent to the closing price per Ordinary Share of 122.6 pence on 21 June 2022 (being the last business day prior to the date of this announcement) and a premium of 1.8 per cent. to the Company’s unaudited Net Asset Value (“NAV”) per Ordinary Share of 114.93 pence as at 31 March 2022.

- The Company is in advanced negotiations to acquire six portfolios, consisting of 27 separate care homes, for a total value of approximately £169 million (the “Pipeline”). Whilst some of these homes can be acquired from the Company’s existing resources, including available debt headroom (after accounting for upcoming capital commitments) of £70 million, as well as new debt to be put in place alongside the acquisitions, the Company will require new equity in order to complete on all the potential opportunities.

- The Company continues to perform strongly and as an owner of UK care homes is supported by several structural benefits including:

- long term, inflation linked, lease structures with the Company benefiting from a WAULT(2) of over 19 years and 98% of its rent roll being linked to RPI (and the remaining 2% linked to CPI), subject to caps and collars;

- a diverse portfolio of 128 different homes (which has grown to 134 properties since the quarter ended 31 March 2022) with an EPRA(3) ‘topped up’ Net Initial Yield at 31 March 2022 of 6.71 per cent as well as sustainable and affordable rents. This is best demonstrated by the Company’s rolling annual average rent cover of 1.9x (to 31 March 2022), demonstrating strong rent protection and its experience since IPO, including during the pandemic, where it has collected 100% of the rent it was due, with no lease variations;

- a portfolio of well-run and financially stable care homes with established care quality and financial track records and tenants who are willing to invest, sometimes alongside the Company, in ensuring high ongoing operational standards in their homes;

- supportive demand fundamentals across the market including increasing requirements from a rapidly ageing population for high quality care and a need to reduce pressure on high-cost, medical care providers in the NHS; and

- a sector that is largely uncorrelated with the wider economy; and

- a disciplined approach to leverage with loan-to-value (“LTV”) of 19.4% (as at 31 March 2022), with a weighted average cost of debt of 3.1% (excluding arrangement fees) and weighted average term to maturity of 6.1 years. The Company’s maximum permitted LTV is 35%.

- The target total dividend for the year to 31 December 2022(1) amounts to 6.54 pence per share and is paid quarterly, which equates to a dividend yield on the Issue Price of 5.6 per cent. The Company has a history of paying covered dividends with the latest 2021 dividend fully covered by EPRA(3) Earnings Per Share (“EPS”) and Adjusted EPS.

- Holders of the New Ordinary Shares being issued pursuant to the issue will be eligible to receive the interim quarterly dividend in respect of the quarter ended 30 June 2022, which is expected to be declared in August 2022.

- Between its IPO on 7 March 2017 and 21 June 2022, the Company has delivered total shareholder returns of 63.3 per cent., equating to an annualised return of 9.7 per cent.

Rupert Barclay, Chairman of Impact Healthcare REIT plc said:

“The portfolio continues to perform well, benefiting from the over-arching defensive characteristics of the care home market, as well our careful selection of homes and tenants with proven financial track records, sustainable rents and facilities which allow for a high quality of care.

The Investment Manager has continued to build a pipeline of investment opportunities which are consistent with the standards of our existing portfolio and allow for more portfolio diversification with some exciting asset management opportunities. Whilst equity capital market conditions remain challenging, this fundraise will allow us to secure a number of attractive investment opportunities and grow our inflation linked long leased REIT for the benefit of all stakeholders.”

Background to the Initial Issue

The Company listed on the London Stock Exchange’s Main Market on 7 March 2017 with an investment objective to provide its shareholders with attractive and sustainable returns through a diversified portfolio of Healthcare Real Estate Assets, with a focus on UK care homes. The Company’s market capitalisation as at 21 June 2022 is approximately £473 million.

The combined committed investment in the portfolio is £565.7 million. This consists of the independently valued portfolio of £484.0 million as at 31 March 2022, alongside a further investment in homes via loans of £48.6 million and committed investments and acquisitions since the quarter end. The portfolio benefits from geographic and tenant diversity, fixed-term leases of typically 20 to 35 years (no break clauses), and rental income which is directly linked to inflation via contractual RPI increases, subject to floors and caps, on 98 per cent. of the leases (the remaining leases are linked to CPI).

The portfolio consists of 134 healthcare properties, of which 130 are care homes and two are NHS assets, as well as two forward funded developments. The Investment Manager has throughout the life of the Company sought to identify opportunities which, as well as offering attractive long-term prospects as standalone care home investments, also offer growth prospects through asset management and development activities including via the refurbishment, extension and development of new beds. During 2022, four asset management projects have been completed with a further fifteen projects either in construction or planning, with a committed capital expenditure of £37 million. Capex has been deployed at an average unlevered yield on cost in excess of c.8% on these projects, which has also served to enhance the environmental and social performance of the portfolio.

The portfolio assets are let under triple net, full repairing and insuring leases, meaning that each tenant is required to pay all taxes, buildings insurance and repair and maintenance costs on the property, in addition to rent. The leases also benefit from several additional, and non-standard, landlord protection clauses which enable the Company to closely monitor each tenant’s rent cover and operational care metrics, as well as empowering the Company to impose strict obligations in the event of declining standards.

The portfolio EPRA(3) ‘topped up’ Net Initial Yield at 31 March 2022 was 6.71 per cent. The Investment Manager is highly selective when choosing the Group’s future homes and tenants, focusing on businesses which it believes are fully aligned with the Company’s investment and ESG objectives and looking on acquisition to set future rents at a level, based upon detailed financial analysis of each home’s historic financial track record, which is both affordable and sustainable over the longer term.

The Company also has a conservative financial approach with a borrowing policy limiting gearing to 35% of gross asset value at the time of borrowing. The Company’s loan-to-value ratio as at 31 March 2022 was 19% with a weighted average cost of debt of 3.1%. With follow on investments after the quarter end, the Company’s loan to value has since increased to approximately 22.8%.

The Company targets an average NAV total return of 9 per cent. per annum over the medium term. However, as a Real Estate Investment Trust, the Company has an income focus demonstrated by its progressive dividend policy under which it seeks to grow its target dividend in line with the inflation-linked rental uplifts received. The target total dividend for the year to 31 December 2022 amounts to 6.54 pence per share(1) and is paid quarterly, which equates to a dividend yield on the placing price of 5.6 per cent. The Company has a history of paying covered dividends with the 2021 dividend fully covered by EPRA(3) EPS and Adjusted EPS.

Pipeline and Use of Proceeds

Despite a competitive acquisition environment, the Company has demonstrated that it can continue to grow its portfolio on accretive terms. Following the Company raising £40 million of new equity in February 2022, it has acquired or exchanged on 10 properties and funded further capital improvements with a combined consideration of £60 million.

The Investment Manager is currently in advanced negotiations in respect of a significant pipeline of assets which meet the Company’s investment objectives, including off-market assets identified through the Investment Manager’s extensive network of industry relationships.

In the near-term, terms have been agreed on six potential acquisitions, which would if completed enable the Company to acquire 27 new care homes for a total consideration of approximately £169 million. The Pipeline includes 2 new tenants with a geographic bias to the South-East of England. The Pipeline portfolios are expected to be acquired at yields and on lease terms similar to the Company’s existing portfolio.

The opportunities available to the Company offer multiple near-term investment options which ensures that the Company can remain highly selective and disciplined with its ongoing growth. The portfolios also differ in size, ranging from an approximate acquisition cost of £10 million up to £60 million, which provides the Company with further acquisition optionality. However, whilst the Investment Manager is confident that the size and nature of the pipeline will provide the Company with extensive investment optionality over the next few months, no contractually binding obligations for the sale and purchase of any of these investment opportunities have yet been entered into.

The Company currently has available headroom under its existing debt facilities which, after adjusting for capital expenditure commitments in 2022, is £70 million.

Given the size of the pipeline, and the requirement for the Company to have certainty of funds in order to enter into binding acquisition agreements, the Board of Directors believe now is an appropriate time to raise new equity.

Benefits of the Issue

The Board believes that proceeding with the Issue will have the following benefits for the Company:

- allow the Company to invest further capital in the Company’s identified pipeline opportunities to enable it to further diversify its existing portfolio and tenant base, and secure value from new and organic follow-on investments;

- spread the Company’s fixed running costs across a larger asset base; and

- increase the size of the Company, which the Investment Manager believes will help make the Company more attractive to: (i) a wider base of counterparties and, therefore, improve the Company’s pipeline of opportunities; and (ii) a wider base of investors and, therefore, improve market liquidity in the Ordinary Shares.

Details of the Placing

Jefferies International Limited (“Jefferies”) and Winterflood Securities Limited (“Winterflood”) are acting as joint global co-ordinators and joint bookrunners to the Company in connection with the Placing (the “Joint Global Co-ordinators”).

The Placing will be made to Qualified Investors (within the meaning of Article 2(e) of the UK version of Regulation (EU) 2017/2019 which is part of UK domestic law by virtue of the EUWA, as amended) (the “UK Prospectus Regulation”) through the Joint Global Co-ordinators subject to the terms and conditions set out in part XV of the Prospectus. By choosing to participate in the Placing and by making an oral and legally binding offer to subscribe for New Ordinary Shares, investors will be deemed to have read and understood this Announcement and the Prospectus in their entirety and to be making such offer on the terms and subject to the conditions in Part XV of the Prospectus, and to be providing the representations, warranties and acknowledgements contained therein.

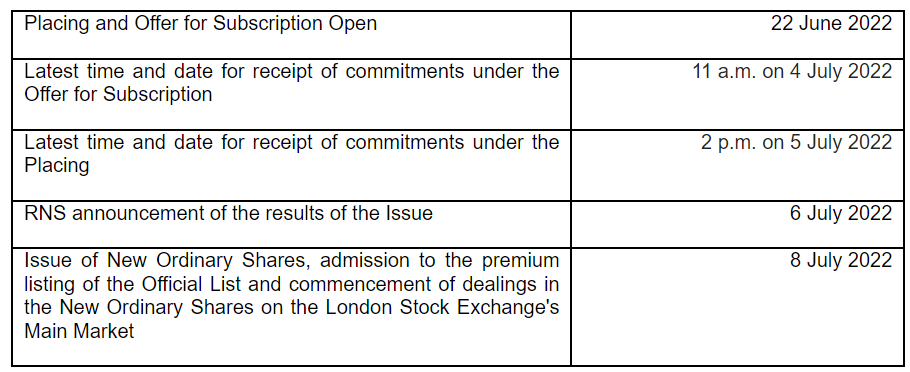

The Placing is expected to close at 2pm. (London time) on 5 July 2022, but may close earlier or later at the absolute discretion of the Company, in consultation with the Joint Global Co-ordinators. The Placing is conditional, inter alia, on the New Ordinary Shares being admitted to listing on the premium listing segment of the Official List of the FCA, and to trading on the main market for listed securities of the London Stock Exchange (together, “Admission”). Subject to Admission becoming effective, it is expected that settlement of subscriptions in respect of the New Ordinary Shares and trading in the New Ordinary Shares will commence at 8.00 a.m. on 8 July 2022, or such later time and/or date as may be announced by the Company.

The allocation of any New Ordinary Shares to any Qualified Investor shall be at the absolute discretion of the Company (in consultation with the Joint Global Bookrunners and the Investment Manager). The Placing is not underwritten. The Company will decide the exact number of New Ordinary Shares to be issued under the Placing on 5 July 2022 taking into consideration the level of demand from investors for New Ordinary Shares and the Company’s ability to invest quickly and efficiently into its existing near term pipeline. It may be necessary to scale back demand from investors for New Ordinary Shares. When doing this, it is intended that New Ordinary Shares issued will be allocated as equitably as possible, with the Directors recognising and taking into their consideration, the importance of pre-emption rights to Ordinary Shareholders. However, for the avoidance of doubt, the Placing is not being conducted on a formal statutory pre-emptive basis and accordingly there can be no guarantee that existing Shareholders wishing to participate in the Placing will receive all of the New Ordinary Shares for which they have applied.

The documents comprising the Prospectus are available for inspection at: https://www.fca.org.uk/markets/primary-markets/regulatory-disclosures/national-storage-mechanism as well as on the Company’s website at www.impactreit.uk/investors/reporting-centre/prospectus

.

Details of the Offer for Subscription

The Board believes it is important to ensure that existing and new retail investors have the opportunity to participate in the Issue and is therefore launching the Offer for Subscription to provide retail investors with the ability to subscribe for New Ordinary Shares in the Issue.

There is a minimum subscription amount of 1,000 New Ordinary Shares at the Issue Price per applicant under the terms of the Offer for Subscription. The Company reserves the right to scale back any order at its absolute discretion, following consultation with the Joint Global Co-ordinators and the Investment Manager. The Company also reserves the right to reject any application for subscription under the Offer for Subscription without giving any reason for such rejection.

The Offer for Subscription is being made under an exemption against the need for an approved prospectus provided for under the Financial Services and Markets Act 2000. As such, no prospectus or offering document has been or will be published pursuant to the UK Prospectus Regulation in connection with the Offer for Subscription, nor will any such prospectus be submitted to be approved by the Financial Conduct Authority.

The Offer for Subscription is only being made in the United Kingdom.

The quantum of the Offer for Subscription shall not exceed the Sterling equivalent of €8.0 million.

The Offer for Subscription is conditional upon Admission of the New Ordinary Shares becoming effective and the Placing Agreement becoming unconditional in all respects in relation to the Placing and not having been terminated on or before Admission.

To participate in the Offer for Subscription, investors should complete the Offer for Subscription form (“Application Form”), which can be found on the Company’s website at https://www.impactreit.uk/investors/reporting-centre/aifmd/, and return it, by post to Computershare Investor Services PLC, Corporate Actions Projects, The Pavilions, Bridgwater Road, Bristol, BS99 6AH (or for applications which are to be paid only by DvP in CREST or by electronic CHAPS bank transfer the Application Form can be sent by PDF by email to impacthealthcare@computershare.co.uk (applications for payments to be made by cheque cannot be accepted by email, as the physical cheque payment needs to accompany the Application Form)), so as to be received by the Receiving Agent by no later than 11 a.m. on 4 July 2022, together in each case with payment in full in respect of the subscription.

The Offer for Subscription is being made on the terms and subject to the conditions set out in the Appendix to this Announcement.

Subject to Admission becoming effective, it is expected that settlement of subscriptions in respect of the New Ordinary Shares and trading in the New Ordinary Shares will commence at 8.00 a.m. on 8 July 2022, or such later time and/or date as may be announced by the Company.

Investors that wish to subscribe for New Ordinary Shares via their broker or platform may do so by requesting their broker or platform subscribe for New Ordinary Shares on their behalf, subject to the terms and conditions between the investor and their broker or platform.

By making an application to subscribe for New Ordinary Shares under the Offer for Subscription, investors will be deemed to have accepted the terms and conditions set out below in the Appendix to this Announcement. An investor that has made an application to subscribe for New Ordinary Shares under the Offer for Subscription accepts that such application shall be irrevocable without the consent of the Board. Upon being notified of its allocation of New Ordinary Shares in the Offer for Subscription, an investor shall be contractually committed to acquire the number of New Ordinary Shares allocated to it at the Issue Price per New Ordinary Share.

Dividend

The New Ordinary Shares issued pursuant to the Issue will, following Admission, rank pari passu in all respects with the existing Ordinary Shares and will carry the right to receive all dividends and distributions declared, made or paid in respect of the Ordinary Shares by reference to a record date after Admission. For the avoidance of doubt, holders of the New Ordinary Shares being issued pursuant to the Issue will be eligible to receive the interim quarterly dividend, in respect of the quarter ended 30 June 2022, which is expected to be declared in August 2022.

Expected Timetable

The dates and times specified above are subject to change. In particular, the Directors may (with the prior approval of Jefferies and Winterflood) bring forward or postpone the closing time and date for the Issue. In the event that a date or time is changed, the Company will notify persons who have applied for Ordinary Shares by post, by electronic mail or by the publication of a notice through a Regulatory Information Service.

Dealing Codes

ISIN of Ordinary Shares

GB00BYXVMJ03

SEDOL of Ordinary Shares

BYXVMJ0

Ticker

IHR

Unless otherwise defined, capitalised terms used in this Announcement shall have the same meaning as set out in the Prospectus published on 27 January 2022 as amended.

Notes

(1) This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

(2) WAULT: Weighted Average Unexpired Lease Term

(3) EPRA: European Public Real Estate Association

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Mahesh Patel

Andrew Cowley

David Yaldron

Jefferies International Limited

Tom Yeadon tyeadon@jefferies.com

Neil Winward nwinward@jefferies.com

Ollie Nott onott@jefferies.com

Tel: +4420 7029 8000

Winterflood Securities Limited

Neil Langford neil.langford@winterflood.com

Joe Winkley joe.winkley@winterflood.com

Tel: +4420 3100 0000

Maitland/AMO (Communications Adviser)

James Benjamin impacthealth-maitland@maitland.co.uk

Alistair de Kare-silver

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

Important Information

This Announcement which has been prepared by, and is the sole responsibility of, Impact Healthcare REIT Plc has been approved for the purposes of section 21 of the Financial Services and Markets Act 2000 (“FSMA”) by Winterflood Securities Limited, which is authorised and regulated by the Financial Conduct Authority.

Shareholders’ capital is at risk and the value of shares and the income from them is not guaranteed and can fall as well as rise due to the performance of the Company and stock market movements. When you sell your investment you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Investors should carefully consider the risks attaching to an investment in the Company, including the risks set out in the ‘Risk Factors’ section below.

This Announcement is an advertisement and does not constitute a prospectus relating to the Company and does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for, any shares in the Company in any jurisdiction nor shall it, or any part of it, or the fact of its distribution, form the basis of, or be relied on in connection with or act as any inducement to enter into, any contract therefor.

Recipients of this announcement who are considering acquiring new ordinary shares in the Company (“New Ordinary Shares”) by participating in the Placing are reminded that any such acquisition must be made only on the basis of the information contained in the Prospectus which may be different from the information contained in this announcement. The documents comprising the Prospectus are available on the Company’s website at https://www.impactreit.uk investors/reporting-centre/prospectus.

Recipients of this announcement who are considering acquiring New Ordinary Shares by participating in the Offer for Subscription are reminded that any such acquisition must be made only on the basis of the Regulatory Information.

This Announcement may not be published, distributed or transmitted by any means or media, directly or indirectly, in whole or in part, in or into the United States. This Announcement does not constitute an offer to sell, or a solicitation of an offer to buy, securities in the United States. The New Ordinary Shares have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “US Securities Act”) or with any securities regulatory authority of any state or other jurisdiction of the United States and the New Ordinary Shares may not be offered or sold, directly or indirectly, within the United States except pursuant to an exemption from the registration requirements of the US Securities Act. There will be no public offer of the New Ordinary Shares in the United States. The New Ordinary Shares are being offered and sold: (i) outside the United States in “offshore transactions” as defined in and in reliance on Regulation S (as defined under the US Securities Act); and (ii) within the United States only to persons reasonably believed to be QIBs, as defined in Rule 144A under the US Securities Act, and that deliver to the Company and the Joint Bookrunners a signed Investor Representation Letter.

Neither this Announcement nor any copy of it may be taken or transmitted into or distributed in any member state of the European Economic Area, Canada, Australia, Japan or the Republic of South Africa or to any resident thereof. Any failure to comply with these restrictions may constitute a violation of the laws of any such jurisdiction. The distribution of this Announcement in other jurisdictions may be restricted by law and the persons into whose possession this Announcement comes should inform themselves about, and observe, any such restrictions.

Jefferies International Limited (“Jefferies”) and Winterflood Securities Limited (“Winterflood”), each of which is authorised and regulated by the FCA in the United Kingdom, is acting only for the Company in connection with the matters described in this announcement and is not acting for or advising any other person, or treating any other person as its client, in relation thereto and will not be responsible for providing the regulatory protection afforded to clients of either Jefferies or Winterflood or advice to any other person in relation to the matters contained herein. None of Jefferies, Winterflood, Impact Health Partners LLP (the “Investment Manager”), nor any of their respective directors, officers, employees, advisers or agents accepts any responsibility or liability whatsoever for this announcement, its contents or otherwise in connection with it or any other information relating to the Company, whether written, oral or in a visual or electronic format.

This Announcement includes statements that are, or may be deemed to be, “forward-looking statements”. These forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “anticipates”, “expects”, “intends”, “may”, “will”, or “should” or, in each case, their negative or other variations or comparable terminology. These forward-looking statements relate to matters that are not historical facts regarding the Company’s investment strategy, financing strategies, investment performance, results of operations, financial condition, prospects and dividend policies of the Company and the assets in which it may invest. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees of future performance. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include, but are not limited to, changes in general market conditions, legislative or regulatory changes, changes in taxation regimes or development planning regimes, the Company’s ability to invest its cash in suitable investments on a timely basis and the availability and cost of capital for future investments.

The Company expressly disclaims any obligation or undertaking to update or revise any forward-looking statements contained herein to reflect actual results or any change in the assumptions, conditions or circumstances on which any such statements are based unless required to do so by the Financial Conduct Authority, the FSMA, the Listing Rules and the Prospectus Regulation Rules made under Part VI of FSMA, the UK version of the Market Abuse Regulation (2014/596/EU) or other applicable laws, regulations or rules.

Neither the content of the Company’s website, nor the content on any website accessible from hyperlinks on its website for any other website, is incorporated into, or forms part of, this announcement nor, unless previously published by means of a recognised information service, should any such content be relied upon in reaching a decision as to whether or not to acquire, continue to hold, or dispose of, securities in the Company.

Risk Factors

Prior to investing in the New Ordinary Shares, prospective investors should consider the associated risks.

The key risks specific to the Company which are known to the Directors are detailed below:

• The effects of COVID-19 over the past two years saw occupancy decline at the Group’s care homes, with the majority of this decline taking place in the first three months of the COVID-19 outbreak, before testing and full levels of personal protective equipment were available to the Group’s care homes. Similar outbreaks of other infectious diseases in the future or further outbreaks of COVID-19, including new variants of COVID-19 could lead to declining occupancy rates at the Group’s care homes and place pressure on the availability of staff. These could in turn have a negative effect on the Group’s results of operations and the Company’s results of operations and financial performance.

• Government may change policy or introduce legislation that affects the UK care sector. The heightened focus on adult social care, and in particular care homes, as a result of COVID-19, has increased the probability of changes to future government policy and a demand for increased funding. Any changes to the legislation applicable to, or the regulatory status of, the Company, the Group’s tenants (“Tenants”) or the Company’s underlying investments, could affect the net incomes received by the Tenants and/or the Company’s ability to provide returns to holders of Ordinary Shares in the Company (“Shareholders”).

• Adverse economic conditions in general are expected to heighten as unemployment levels rise and the government implements measures to reduce the unprecedented level of debt that has been required to manage the immediate economic implications of the COVID-19 pandemic. Adverse market conditions in the healthcare sector in particular, and their impact on the Tenants, may have a material adverse effect on the Tenants’ covenant strength and ability to meet their rent payment obligations resulting in an increase in the portfolio default rate, received yield on investment and, therefore, cash flows.

• A weakening of the UK care market could materially affect Tenants’ covenant strength and their ability to pay rent, resulting in a reduction in the value of the care home and a higher risk of default, which in turn may impact on the yields received from the Portfolio and, in turn, on the timing of distributions paid to Shareholders.

• The default of one or more Tenants, or failing to act quickly and decisively when confronted with a failing Tenant, would affect the value of the Group’s homes and both the Company’s ability to pay dividends and to meet its financing obligations.

• If a Tenant fails to adequately repair and maintain the properties it leases, in accordance with the agreed annual repair and maintenance budget, the effect on the quality and reputation of the affected care home could result in negative business prospects for that care home, leading to reduced bed occupancy and/or increased future maintenance costs. This could materially adversely affect the Company’s financial position, results of operations and business prospects.

• Tightening environmental regulations may increase the need for investment or redevelopment of the portfolio of properties held directly or indirectly by the Company from time to time (“Portfolio”) and restrict Tenants’ ability to provide care and earn revenue. Failure to consider the effects of climate change could accelerate the obsolescence of the Group’s care homes (both physical and low carbon transition risks) with corresponding implications to value and long-term income generation.

• There is no guarantee that any borrowings of the Company or any subsidiary of it that has incurred or incurs borrowings, if applicable, will be able to be refinanced on their maturity either on terms that are acceptable to the Company or at all. If the Group is unable to operate within its debt covenants, this could lead to a default and the Group’s debt funding being recalled.

• The Company relies on key individuals at the Investment Manager to identify and select investment opportunities, however, there can be no assurance as to these individuals’ continued service. The death or departure of any of these individuals without adequate replacement may have a material adverse effect on the Company’s business prospects and results of operations.

• The Company’s investment objective requires it to invest in a portfolio of healthcare real estate assets; new assets may not be available on the terms required to generate the Target Dividend and Target Total Return, or at all. Market conditions may restrict availability and have a generally negative impact on the Company’s ability to identify and execute future investments in suitable assets that might generate acceptable returns. To the extent that there is a delay in making investments while the Company has capital available to deploy, there is greater likelihood that the Group’s growth in underlying earnings will be limited and the Company’s ability to make distributions to Shareholders will be adversely affected.

• The Company may be faced with competition in securing assets. To the extent that the Company does not utilise the net proceeds of the Initial Issue or a subsequent placing under the Placing Programme to repay debt, this could result in the Company taking longer than anticipated to invest the proceeds of the Initial Issue or future placing under the Placing Programme. Delay in deployment into investments may also result in the price of certain assets increasing. As such, competition in securing assets may have an adverse impact on the amounts that are able to be returned to shareholders by way of a dividend as well as the net asset value of the Company.

The key risks associated with an investment in the New Ordinary Shares which are known to the Directors are detailed below:

• The value of the New Ordinary Shares and the income derived from those shares (if any) can fluctuate and may go down as well as up. The New Ordinary Shares may trade at a discount to their net asset value.

• It may be difficult for Shareholders to realise their investment and there may not be a liquid market in the New Ordinary Shares.

• If the Directors decide to issue further shares (including pursuant to the Placing Programme), the proportions of the voting rights held by Shareholders who do not participate in such share issues pro rata to their prior shareholdings will be diluted.

Information to Distributors – Product Governance

Solely for the purposes of the product governance requirements of Chapter 3 of the FCA Handbook Product Intervention and Product Governance Sourcebook (the “UK Product Governance Requirements”), and/or any equivalent requirements elsewhere to the extent determined to be applicable, and disclaiming all and any liability, whether arising in tort, contract or otherwise, which any manufacturer (for the purposes of the UK Product Governance Requirements and/or any equivalent requirements elsewhere to the extent determined to be applicable) may otherwise have with respect thereto, the New Ordinary Shares the subject of the Issue have been subject to a product approval process, which has determined that such New Ordinary Shares are: (i) compatible with an end target market of retail investors and investors who meet the criteria of professional clients and eligible counterparties, each defined in Chapter 3 of the FCA Handbook Conduct of Business Sourcebook; and (ii) eligible for distribution through all permitted distribution channels (the “Target Market Assessment”).

Notwithstanding the Target Market Assessment, distributors should note that: the price of the Ordinary Shares may decline and investors could lose all or part of their investment; the Ordinary Shares offer no guaranteed income and no capital protection; and an investment in the Ordinary Shares is compatible only with investors who do not need a guaranteed income or capital protection, who (either alone or in conjunction with an appropriate financial or other adviser) are capable of evaluating the merits and risks of such an investment and who have sufficient resources to be able to bear any losses that may result therefrom. The Target Market Assessment is without prejudice to any contractual, legal or regulatory selling restrictions in relation to the Issue. Furthermore, it is noted that, notwithstanding the Target Market Assessment, the Joint Bookrunners will only procure Placees who meet the criteria of professional clients and eligible counterparties.

For the avoidance of doubt, the Target Market Assessment does not constitute: (a) an assessment of suitability or appropriateness for the purposes of Chapters 9A or 10A respectively of the FCA Handbook Conduct of Business Sourcebook; or (b) a recommendation to any investor or group of investors to invest in, or purchase, or take any other action whatsoever with respect to the Ordinary Shares.

Each distributor is responsible for undertaking its own target market assessment in respect of the Ordinary Shares and determining appropriate distribution channels.

UK PRIIPs Regulation

In accordance with the UK version of Regulation (EU) No. 1286/2014 on key information documents for packaged retail and insurance-based investment products, which is part of UK law by virtue of the European Union (Withdrawal) Act 2018, as amended (the “UK PRIIPs Regulation”) a key information document (“KID”) in respect of an investment in Ordinary Shares has been prepared by the Company and is available to investors at https://www.impactreit.uk/investors/reporting-centre/aifmd/.

If you are distributing New Ordinary Shares, it is your responsibility to ensure that the KID is provided to any clients that are “retail clients”.

The Company is the only manufacturer of Ordinary Shares for the purposes of the UK PRIIPs Regulation and none of Jefferies, Winterflood or the Investment Manager are manufacturers for these purposes. None of Jefferies, Winterflood or the Investment Manager makes any representations, express or implied, or accepts any responsibility whatsoever for the contents of the KID prepared by the Company nor accepts any responsibility to update the contents of the KID in accordance with the UK PRIIPs Regulation, to undertake any review processes in relation thereto or to provide the KID to future distributors of Ordinary Shares. Each of Jefferies, Winterflood or the Investment Manager and their respective affiliates accordingly disclaim all and any liability whether arising in tort or contract or otherwise which it or they might have in respect of any key information document prepared by the Company. Investors should note that the procedure for calculating the risks, costs and potential returns in the KID are prescribed by laws. The figures in the KID may not reflect actual returns for the Company and anticipated performance returns cannot be guaranteed.

For full appendix, please see the regulatory news page.