The board of Directors (the “Board“) of Impact Healthcare REIT plc (ticker: IHR), the real estate investment trust which gives investors exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, is pleased to provide the following business and trading update for the quarter to 30 September 2022.

NET ASSET VALUE

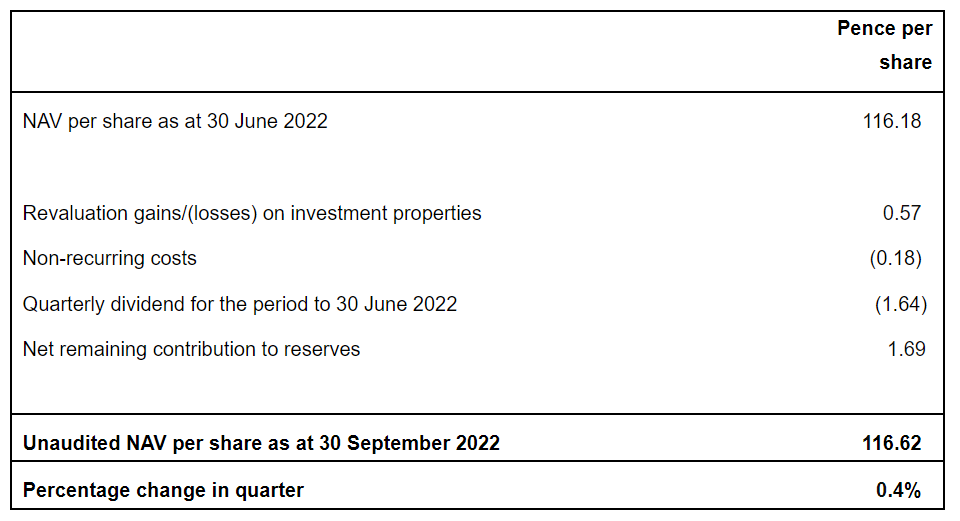

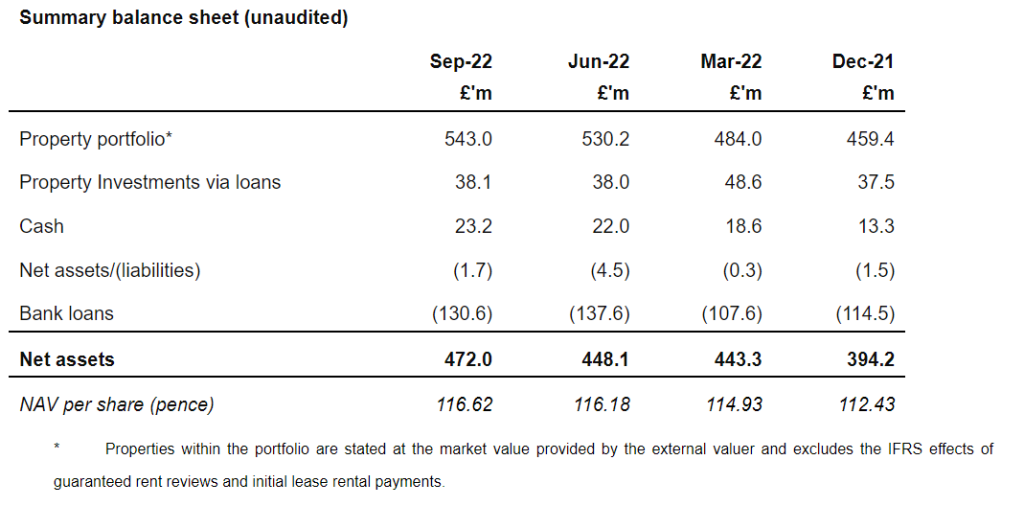

- The unaudited net asset value (“NAV“) as at 30 September 2022 was £472.0 million, 116.62 pence per share, representing increases on the previous quarter of 5.3% and 0.4%, respectively (NAV as at 30 June 2022 of £448.1 million, 116.18 pence per share).

- The NAV attributable to the ordinary shares of the Company is calculated under International Financial Reporting Standards (“IFRS“) and incorporates the independent portfolio valuation at 30 September 2022 and net income for the period. The EPRA Net Tangible Assets at 30 Sep 2022 was 116.46 pence per share; the difference to the IFRS NAV reported above is due to the value of the Group’s interest rate cap.

UNAUDITED TOTAL ACCOUNTING RETURN AND DIVIDEND DECLARATION

- The unaudited total accounting return for the quarter was 1.8%, comprising dividends paid in the quarter of 1.635 pence per share and 0.44 pence per share growth in NAV.

- The Board has today declared for the period an interim dividend of 1.635 pence per ordinary share, payable on 25 November 2022 to shareholders on the register on 4 November 2022. The ex-dividend date will be 3 November 2022. This dividend will be paid as a Property Income Distribution (“PID“). The dividend for the quarter remains fully covered on both an EPRA earnings and adjusted earnings basis.

- This is in line with the Company’s annual dividend target of 6.54 pence per share for the year ending 31 December 2022(1), a 2.0% increase over the 6.41 pence in dividends paid per ordinary share for the year ended 31 December 2021.

FINANCING

- The Group’s conservative financing and investment strategy means the Group is well placed to manage the current environment of rising interest rates.

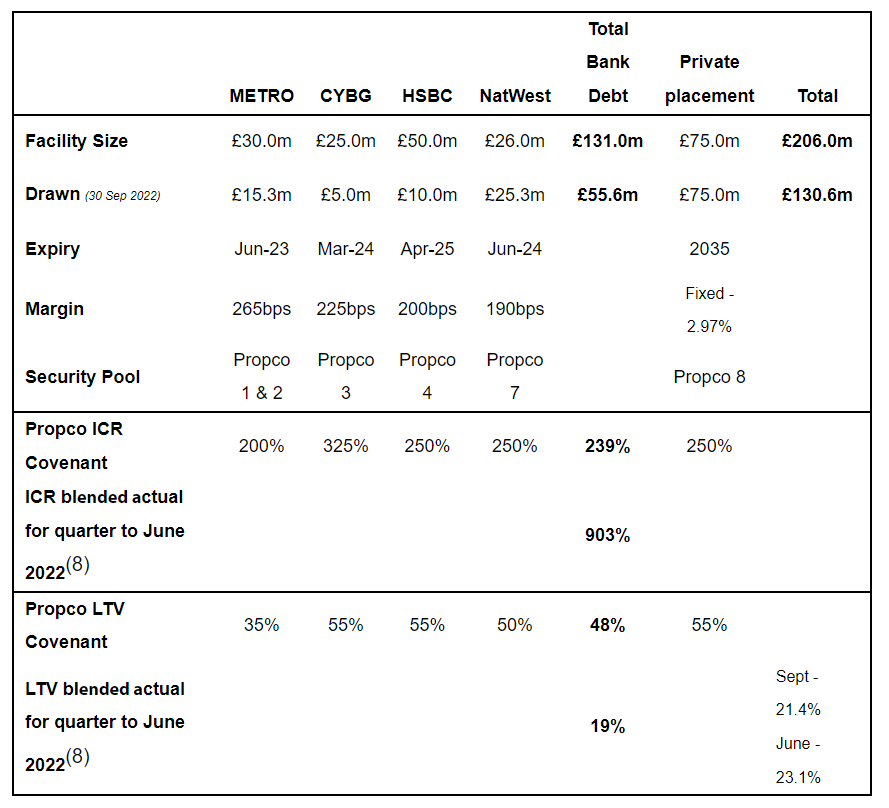

- The Group’s gross loan to value ratio was 21.4% as at 30 September 2022 (at 30 June 2022: 23.1%). The Group has total available debt facilities of £206 million, of which £131 million is currently drawn.

- 77% of the Group’s drawn debt at 30 September 2022 is hedged via a £75 million long term debt facility expiring in 2035 fixed at just under 3.0%, and a £25 million interest rate cap of 1% which expires in June 2023.

- The Group’s weighted average cost of drawn debt at 30 September 2022 was 3.9% and weighted average term of debt was 5.8 years

- At current drawn debt levels alongside current hedging facilities, a further 100 bps rise in underlying interest rates would result in a 23 bps increase in our weighted average cost of debt. In the quarter to September 2022 an increase of 100 bps in underlying interest rates would have resulted in a reduction in underlying earnings of 0.02 pence per share.

- In addition, the Group is delivering a covered dividend on adjusted earnings, which is a proxy for cash earnings of the Group.

- The Group benefits from long-term leases with 100% of its rental income linked to inflation (with floors and caps), which will allow the Group to mitigate rising interest costs.

- As highlighted in the table below, our current bank debt facilities at 30 June 2022 had a blended interest cover at the Propco level of over 900% against a blended interest cover covenant of 239% and a blended LTV of 19% against a blended LTV covenant at the Propco level of 48%(2). The Group also has unsecured assets and cash of £52.9 million as at 30 September 2022. The Group’s maximum permitted LTV at Group level continues to be 35%.

- We are in advanced discussions on refinancing of our RCF facilities. In addition the Group can repay the Metro facility, which expires in June 2023, from available headroom on its remaining facilities.

- The Company also successfully raised gross proceeds of £22.3 million in the period through an equity raise in July 2022.

TENANT PERFORMANCE

- While the headwinds threatening the United Kingdom economy gained in strength during the third quarter, the Group’s tenants have also benefited from the tailwinds created by the supportive, long-term fundamentals of the sector in which they operate. Demand for their services is needs based, not wants based, and hence is not directly correlated to wider economic conditions. During the quarter the Group’s tenants have seen their occupancy ratios continue to recover towards pre-pandemic levels, with strong growth in the underlying fees they charge for the care they provide; and they have been managing underlying cost pressures effectively.

- At 30 June 2022, rent cover was 1.85x for the past 12 months, and 1.73x in the second quarter. The Investment Manager has received trading data for 88% of the portfolio for the months of July and August but has not yet received the full data for the quarter ending 30 September 2022. Based on early indications from the July and August data, rent cover in the third quarter is expected to be higher than in the second quarter.

- Occupancy(3) at 30 September 2022 was 87.3%, up 1.9% on 30 June 2022 (85.4%). Occupancy was 89.2% in March 2020, at the beginning of the COVID pandemic. It hit a low point of 78.7% during the second wave of the pandemic in January 2021. Tenants report a strong level of enquiries for available beds and are more confident at being able to satisfy this demand as lockdown provisions on care homes have now mostly been lifted.

- Average weekly fees charged by the Group’s tenants for providing care have been increasing in line with inflation. Across the Group’s portfolio, average weekly fees were £911 in August 2022, up 10.7% on the average for the third quarter of 2021. During the COVID pandemic care providers received infection control grants from the government, but these grants have now tailed off. In July and August they accounted for 0.1% of the Group’s tenants’ revenues(4).

- Staff costs have been rising, but have remained stable as a percentage of our tenant revenues at 64% as occupancy gains and fee increases have grown those revenues. Our tenants did mostly report a spike in the use of temporary agency staff during the first quarter of 2022 and are focusing on reducing temporary staff with increased overseas recruitment. Agency costs for the 8 months to August 2022 represented 13% of our tenants’ staff costs on average across our portfolio(4).

- Utility and food costs are increasing but at manageable levels. Food costs were 3.7% of revenues in the 8-month period to 31 August 2022(4) up from 3.6% of revenues in the year to December 2021. Utility costs were 2.5% of revenues in the 8-month period to 31 August 2022(4) up from 2.0% of revenues in the year to December 2021.

- As at 19 October 2022, 78% of the homes owned by the Group were rated Good or Outstanding by the Care Quality Commission in England (or the equivalent regulators in other parts of the United Kingdom) based on the quality of care provided by the Group’s tenants.

- The Group continues to receive 100% of rent payments as they fall due with no lease variations.

PROPERTY VALUATION AND PORTFOLIO UPDATE

- While the wider market backdrop has become substantially more uncertain, the Group’s independent valuer has found no reason as at 30 September 2022 to justify a shift in the investment yields used to value healthcare real estate. Therefore there has been no material movement as at 30 September in the underlying valuation yields of the Group’s property investments (“Portfolio”) applied by the independent valuer. The Portfolio was independently valued at £543.0 million as at 30 September 2022 (valuation as at 30 June 2022: £530.2 million). This represents a 0.8% increase in value on a like-for-like basis in the quarter, and a total increase of 2.4% over that period, including the acquisition of three homes.

- £3.7 million of this related to assets with rent reviews, a 0.7% increase in value on a like-for-like basis. 12 rent reviews were completed in the quarter at an average uplift of 4.69% per annum in line with the rental increase cap on these leases.

- £(1.4) million was from yield movements due to underlying performance of the homes a 0.3% decrease in value on a like-for-like basis.

- £1.9 million related to capital expenditure on existing properties a 0.4% increase in value on a like-for-like basis.

- The Group also completed on the acquisition of three homes in Scotland with 155 beds, for £8.1 million. The homes are being operated by an existing tenant, Silverline.

- The Portfolio EPRA ‘topped up’ Net Initial Yield at 30 September 2022 was 6.68% (30 June 2022 6.69%).

- 100% of the Group’s rental income is linked to inflation, with 84%(7) of the Group’s leases linked to RPI with a floor and cap at 2% p.a. and 4% p.a., 15% linked to RPI with a floor and cap at 1% p.a. and 5% p.a. and 1% with an annual CPI uplift.

- The Group also announced in the quarter that it had exchanged contracts to acquire two care homes with 168 beds with a new tenant, Belmont Healthcare (“Belmont“), the Group’s 14th tenant(5).

- In addition to the portfolio value above, the Group has an investment by way of a loan to Holmes Care Group in 12 homes with 480 beds valued at £38.1 million.

- Contracted rent increased to £43.2 million(6) at the quarter end (at 30 June 2022: £42.0 million) an increase of 2.7%. This increase was as a result of the Group’s commitment to a portfolio of two new homes with Belmont, and the 12 rent reviews during the period, as discussed above.

- At 30 September 2022, the Portfolio comprised 136 healthcare properties(7), of which 134 are care homes let to 13 tenants(4) on fixed-term leases of 20 to 35 years (no break clauses)(8), subject to annual upward-only Retail Price Index-linked rent reviews (with a floor and cap at 2% p.a. and 4% p.a., respectively on 113 leases, and 1% p.a. and 5% p.a. on 21(8)). In addition, the Group owns two healthcare facilities leased to the NHS with annual CPI uplift. In total, the Group had 14 tenants(5) across its Portfolio.

- The weighted average unexpired lease term across the Portfolio was 19.7 years as at 30 September 2022.

- Just after the quarter end, the Group also successfully continued its active management of the portfolio with the sale of one non-core home with 68 beds for 4% above the 30 June 2022 book value.

Notes:

(1) This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

(2) These exclude the fixed long term debt, and the interest rate cap of 1.0% for £25 million of debt, which is independent of but linked to the Metro bank debt.

(3) Excludes three turn-around assets that have not reached maturity.

(4) Based on tenant trading data for 88% of our portfolio to 31 August 2022.

(5) Minster and Croftwood (both subsidiaries of Minster Care Group), Careport, Prestige, Renaissance, Welford, Maria Mallaband Countrywide Group, NHS Cumbria, Optima, Holmes Care, Silverline, Electus Healthcare and Carlton Hall. In the period, the Group to acquire two properties with a new tenant, Belmont.

(6) Contracted rent includes all post tax income from investment in properties, whether generated from rental income or post tax interest income.

(7) Includes exchanged and under constructions assets.

(8) 12 homes are currently funded via a loan with the option to acquire and enter into a fixed term lease with a floor of 1% and a cap of 5%.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Andrew Cowley

Mahesh Patel

David Yaldron

Jefferies International Limited

Tom Yeadon

Neil Winward

Ollie Nott

Tel: +4420 7029 8000

Winterflood Securities Limited

Neil Langford

Joe Winkley

Tel: +4420 3100 0000

H/Advisors Maitland (Communications Adviser)

James Benjamin impacthealth-maitland@maitland.co.uk

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

NOTES:

Impact Healthcare REIT plc acquires, renovates, extends and redevelops high quality healthcare real estate assets in the UK and lets these assets on long-term full repairing and insuring leases to high-quality established healthcare operators which offer good quality care, under leases which provide the Company with attractive levels of rent cover.

The Company aims to provide shareholders with an attractive sustainable return, principally in the form of quarterly income distributions and with the potential for capital and income growth, through exposure to a diversified and resilient portfolio of UK healthcare real estate assets, in particular care homes for the elderly.

The Company has a progressive dividend policy with a target to grow its annual aggregate dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year.

On this basis, the target total dividend for the year ending 31 December 2022 is 6.54 pence per share1, a 2.0% increase over the 6.41 pence in dividends paid or declared per ordinary share for the year ended 31 December 2021.

The Group’s Ordinary Shares were admitted to trading on the main market of the London Stock Exchange, premium segment, on 8 February 2019. The Company is a constituent of the FTSE EPRA/NAREIT index.