Half year results for the six months ended 30 June 2022

Dividend declaration

CONTINUING STRONG AND RESILIENT PERFORMANCE

The Board of Directors of Impact Healthcare REIT plc (ticker: IHR), the real estate investment trust which gives investors exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, today announces the Company’s half year results for the six months ended 30 June 2022 and declares the Company’s second quarter interim dividend of 1.635 pence per ordinary share.

This dividend is for the period from 1 April 2022 to 30 June 2022 and is payable on 9 September 2022 to shareholders on the register on 26 August 2022. The ex-dividend date will be 25 August 2022. This dividend will be a property income distribution dividend (“PID”). This dividend is in line with the aggregate total dividend target of 6.54 pence per share¹ for the year ending 31 December 2022.

Rupert Barclay, Chairman of Impact Healthcare REIT plc, commented:

“We are a responsible long-term owner of a diversified and resilient portfolio of well run and financially stable care homes that have established care quality and financial track records. We lease them on long-term leases to tenants who we partner with to ensure high ongoing operational standards and care.

Against a challenging and uncertain backdrop, our business continues to demonstrate its high level of in-built resilience, underpinned by a sector that is largely uncorrelated with the wider economy. This is demonstrated by our 100% collection of rent since our IPO in March 2017, with no lease variations, and a healthy rolling 12-month rent cover of 1.85x². This underlines our tenants’ ability to manage the inflationary challenges in the current economic environment.

This has helped us to deliver a strong set of results for the first half of 2022, with our NAV per share up 3.3% and NAV up 13.7% since 31 December 2021, profit before tax up 88% on the same period in 2021, and progressive inflation-linked dividends declared for the period well covered by earnings. We delivered a total accounting return for the six-month period of 6.2%, and we are well placed to deliver our 9% per annum medium-term total accounting return target¹.

These robust results are primarily driven by the market value uplifts received on our portfolio, underpinned by our inflation-linked rent reviews, stable operator performance and our maintenance of a conservatively managed balance sheet.

The Group is well positioned to continue to deliver attractive sustainable returns to shareholders through its covered progressive dividend, further strong capital growth potential and value creation capabilities of our resilient portfolio for the benefit of all our stakeholders.”

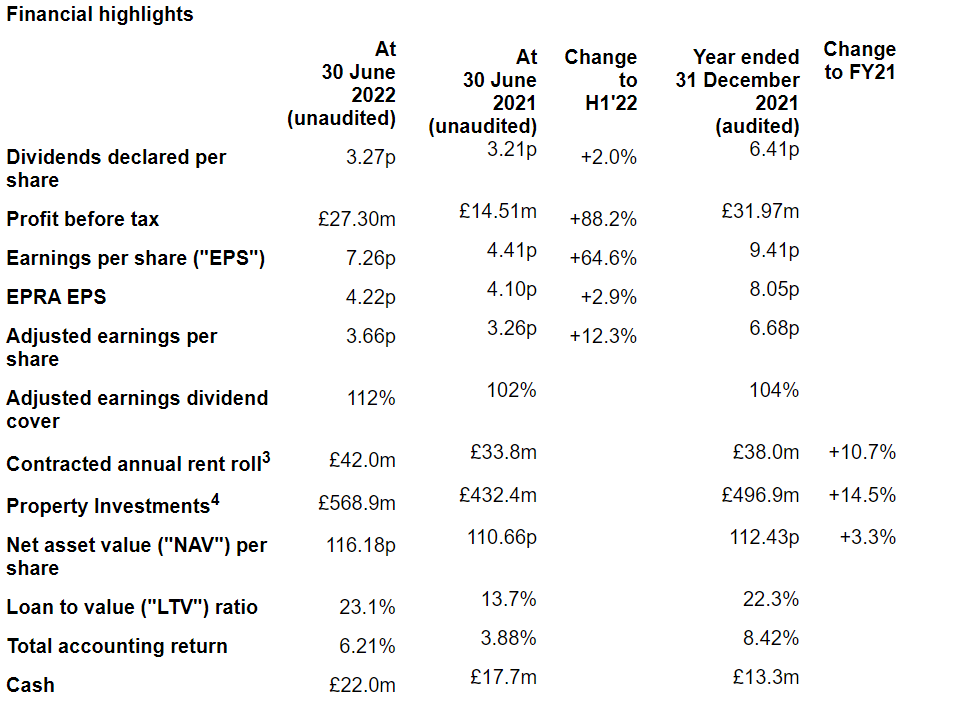

- The unaudited NAV at 30 June 2022 was £448.1 million (+13.7%) or 116.18 pence per share (+3.3% increase) (31 December 2021: NAV: £394.2 million; 112.43 pence per share). This increase is primarily driven by the market value uplifts received on the property portfolio, underpinned by the inflation-linked rent reviews and stable operator performance.

- Total accounting return for the six months to 30 June 2022 was 6.21%, comprising dividends paid in the period of 3.24 pence and NAV growth of 3.75 pence per share (+3.3%) in the period. As a result, we are well placed to deliver against our 9% per annum medium-term total accounting return target¹.

- Our property investments were independently valued at £568.9 million (note 4) as at 30 June 2022, a 14.5% increase from £496.9 million on 31 December 2021. On a like-for-like basis the portfolio increased by 4.9% (£22.6 million) between 31 December 2021 and 30 June 2022, driven mainly by the inflationary rental uplifts and capital value improvements from our asset management activities.

- The market value uplift of investment properties was £13.4 million (H1 2021: £5.0 million), contributing to profit before tax increasing by 88.2% to £27.3 million (H1 2021: £14.5 million).

- The Company declared two quarterly dividends of 1.635 pence for the period, in line with the Company’s annual dividend target of 6.54 pence per share for the year to 31 December 2022¹, an increase of 2.0% on the dividend paid in 2021 of 6.41 pence per share.

- Dividends declared for the period were 129% covered by EPRA earnings per share and 112% by adjusted earnings per share.

- EPS increase of 64.6% to 7.26 pence per share (H1 2021: 4.41 pence per share) (basic and diluted) owing to a 24.2% increase in contracted annual rent on H1 2021 and a 2.9% uplift in the investment portfolio’s value during the period, following the inflation-linked rent increases and asset management activities in the first half of 2022.

- Adjusted EPS rise of 12.3% to 3.66 pence per share (H1 2021: 3.26 pence per share), a result of increased cash revenue from rent reviews and the use of moderate leverage to further scale property investments.

- Grew our annual contracted rent roll³ by 10.7% to £42.0 million (31 December 2021: £38.0 million); this consisted of:

- Acquisition of five new properties and exchange of contracts to acquire a further three properties, contributing £3.0 million to the contracted annual rent.

- 79 properties had rent reviews during the period adding £872k to the contracted annual rent, representing a 4.0% increase on the associated portfolio over the six months to 30 June 2022.

- New capex commitments during the period adding a further £68k to contracted annual rent.

- Drew down the second tranche of long-term institutional debt amounting to £38 million, maturing in June 2035 at an attractive fixed coupon of 3.0%.

- The Group now has £206.0 million of committed debt facilities. Our drawn debt as at 30 June 2022 was £137.6 million, giving us a gross LTV of 23.1%, with significant headroom to our borrowing policy cap of 35%. £75.0 million of this is long-term fixed-rate debt with a weighted average coupon of 2.967% and maturing in 2035. As at 30 June 2022, the weighted average term of debt facilities (excluding options to extend) was 6.1 years.

- 48% of our debt facilities are currently hedged against rising interest rate costs (73% of drawn debt as at 30 June 2022). 36% through long-term fixed-rate facilities and 12% through an interest rate cap at 1% which expires in June 2023.

- £40.0 million of gross proceeds from placing of new ordinary shares, admitted onto the main market of the London Stock Exchange on 21 February 2022. A further £22.3 million of gross proceeds was raised from a placing of new ordinary shares following the period end. These shares were admitted onto the main market of the London Stock Exchange on 8 July 2022.

- Following the post-period equity raise, the Company has over £110 million in available funds for existing capital commitments and to fund further pipeline investment opportunities.

- The Group continued to demonstrate the resilience of its business model, collecting 100% of rent due for the period, with no changes to any lease terms or payment schedules, and the portfolio continues to have zero voids.

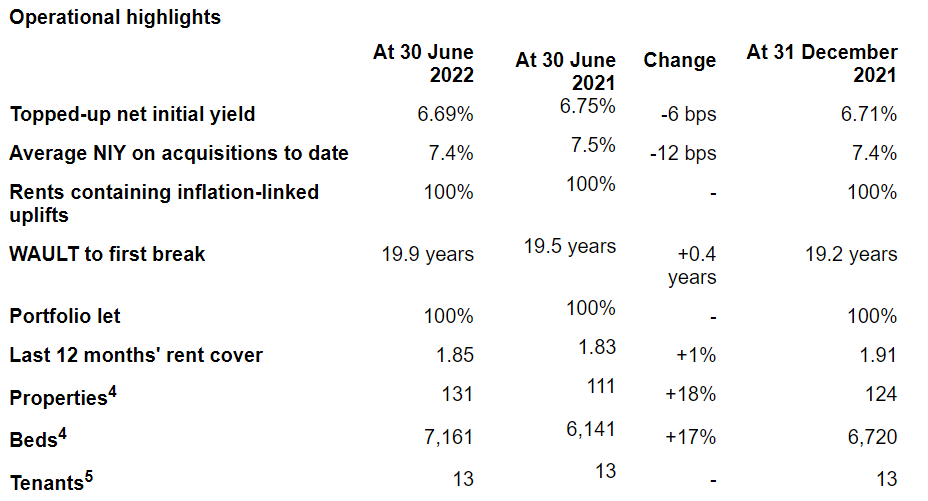

- Throughout the period our tenants have continued to perform well with average rent cover for the 12 months to 30 June 2022 at 1.85x.

- Occupancy continued to climb across the Group’s homes to 85.4% (note 6) by the period end, up 2.3% on the year (31 December 2021: 83.1%), and the highest it has been since early 2020.

- Acquired seven properties and exchanged contracts on a portfolio of three properties, in total adding 596 beds for a total net consideration of £55.2 million.

- At 30 June 2022, the Group had invested in 131 properties with 7,161 beds, up from 124 and 6,720, respectively, at 31 December 2021 (note 4).

- The Group also exchanged contracts to acquire a further three homes in the period, which once completed will bring the total portfolio investments to 134 properties, which offer 7,316 beds (note 4).

- Our portfolio represents approximately 1.5% of a highly fragmented UK market (with an estimated 465,000 beds for elderly care in total). We remain confident that we can continue to grow while being very selective in looking for acquisitions which will be accretive and will further increase diversification.

- All leases continue to be inflation-linked with upward-only rent reviews. We also cap the rental uplifts to avoid putting undue strain on our tenants, which helps to create sustainable long-term income.

- Weighted average unexpired lease term (“WAULT”) of 19.9 years at 30 June 2022 (30 June 2021: 19.5 years).

- EPRA ‘topped up’ net initial yield of 6.69% as at 30 June 2021 (30 June 2021: 6.75%). The average net initial yield of our acquisitions to date was 7.4%.

- Asset management remains a key focus of our business, enhancing the quality, sustainability and value creation capabilities of our portfolio, working in partnership with our tenants to ensure high ongoing operational standards in our homes for the benefit of all our stakeholders.

- In the period, we completed the internal refurbishment of Belmont House in Harrogate and the upgrade of three care homes operated by our tenant, Electus Healthcare, in Northern Ireland.

- Good progress has been made on site in Carlisle at Riverwell Beck, formerly known as Blackwell Vale, whereby we have undertaken a comprehensive refurbishment and extension of the existing care home, enhancing the common areas, facilities and services, and increasing operational capacity from 51 to 57 beds, adding six en-suite bedrooms and a further three en-suite wet rooms to existing bedrooms.

- Looking ahead, in Bristol, phase one of the new link building at Fairview House and Fairview Court is targeting completion next month. Phase two will then commence, which involves an extensive refurbishment of Fairview House and the introduction of further sustainability improvement measures to improve the EPC rating of the property to an overall EPC rating of A.

- We have a number of future capital projects in either the planning or tender phase, which we will look to commit to over the next six-month period; the average yield on cost is expected to be 8%.

- Our forward-funded development in Hartlepool has achieved practical completion. The 94-bedroom home will be operated by Prestige, one of the Group’s existing tenants, and will offer a modern and well-designed environment for residents. The Group funded development costs of £6.1 million, the project will deliver an initial yield on development costs of 7.8%, and in the period has received a valuation uplift of £1.9 million.

Enhancing the social environment of our homes and their environmental performance is fundamental to long-term value creation

Our homes provide an important service in their communities, providing accommodation and associated support for a vulnerable segment of society. We work closely with our tenants to ensure they can provide an enjoyable, safe, caring and energy efficient environment that can enhance the wellbeing of their residents. In the period we have:

- Published our EPRA sustainability report for 2021;

- Progressed identified opportunities to improve energy efficiency and EPC ratings;

- Commenced work on assessing the greenhouse gas emissions from our portfolio in advance of developing a net zero carbon strategy;

- Progressed work to assess our transitional and physical climate risk and opportunity in order to report under TCFD this year; and

- Commenced work on how we can understand and measure the clear inherent social value embedded in our portfolio.

Notes

1 This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

2 Includes the benefit of grant income, which largely ended in March 2022 and is beginning to unwind.

3 Contracted rent includes all post-tax income from investment in properties, whether generated from rental income or post-tax interest income.

4 This relates to the property portfolio along with property portfolios that have been invested in via loans to operators with an option for the Group to acquire.

5 Including Croftwood and Minster, which are both part of the Minster Care Group.

6 Excludes three turn-around assets that have not reached maturity.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Andrew Cowley

Mahesh Patel

David Yaldron

Jefferies International Limited

Tom Yeadon

Neil Winward

Ollie Nott

Tel: +4420 7029 8000

Winterflood Securities Limited

Neil Langford

Joe Winkley

Tel: +4420 3100 0000

Maitland/AMO (Communications Adviser)

James Benjamin impacthealth-maitland@maitland.co.uk

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

NOTES:

Impact Healthcare REIT plc acquires, renovates, extends and redevelops high-quality healthcare real estate assets in the UK and lets these assets on long-term full repairing and insuring leases to high-quality established healthcare operators which offer good quality care, under leases which provide the Company with attractive levels of rent cover.

The Company aims to provide shareholders with an attractive sustainable return, principally in the form of quarterly income distributions and with the potential for capital and income growth, through exposure to a diversified and resilient portfolio of UK healthcare real estate assets, in particular care homes for the elderly.

The Company has a progressive dividend policy with a target to grow its annual aggregate dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year.

On this basis, the target total dividend for the year ending 31 December 2022 is 6.54 pence per share*, a 2.0% increase over the 6.41 pence in dividends paid per ordinary share for the year ended 31 December 2021.

The Group’s Ordinary Shares trade on the main market of the London Stock Exchange, premium segment. The Company is a constituent of the FTSE EPRA/NAREIT index.

* This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

Half year results presentation

The Company presentation for investors and analysts will take place at 8.30am (UK) today via a live webcast and conference call.

To access the live webcast, please register in advance here:

https://www.lsegissuerservices.com/spark/ImpactHealthcareREIT/events/59df34ab-a55f-4f99-bc23-963fc7d1ee0b

To access the live conference call, please register to receive unique dial-in details here:

https://cossprereg.btci.com/prereg/key.process?key=PTHLAVCCE

The recording of the results presentation will be available later in the day via the Company’s London Stock Exchange profile page:

https://www.lsegissuerservices.com/spark/ImpactHealthcareREIT/events/59df34ab-a55f-4f99-bc23-963fc7d1ee0b

and from the Company website: https://www.impactreit.uk/investors/reporting-centre/presentations/

For the full RNS please see the attached document.