Delivered a strong financial and operational performance, benefiting from the resilience and growth of the portfolio and the annual rental increases inherent in the leases, resulting in a fully covered growing dividend

Impact Healthcare REIT plc (ticker: IHR), the real estate investment trust which gives investors exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, is pleased to announce its full year results for the 12 months ended 31 December 2021.

Rupert Barclay, Chairman of Impact Healthcare REIT PLC, commented:

“We have deliberately fostered our resilience by carefully selecting tenants, putting in place leases with robust rent cover and inflation linkages and maintaining a prudent balance sheet. Our tenants have provided high-quality care during the pandemic and in turn we have received 100% of the rent due. This has underpinned a fully covered dividend for 2021.

As we emerge from the pandemic, the long-term investment case for care homes is unchanged. Occupancy is expected to continue to recover while the support from government grant funding falls away. Demographic trends and the rising incidence of specialist needs, such as dementia, will continue to drive demand for care, which will require many new beds, in suitable homes, to be added to the market. The Government’s reforms will provide additional funding for the sector and contribute to its resilience.

We have a good level of protection against the current inflationary environment, through the upwards-only index-linked rent reviews in our leases.

We have a strong pipeline of accretive acquisitions, which has the potential to add attractive new assets and further tenants to the portfolio. We are also exploring further asset management and development opportunities, with a view to enhancing shareholder returns. We therefore look forward to making further progress with our growth strategy during 2022 and for the long term.”

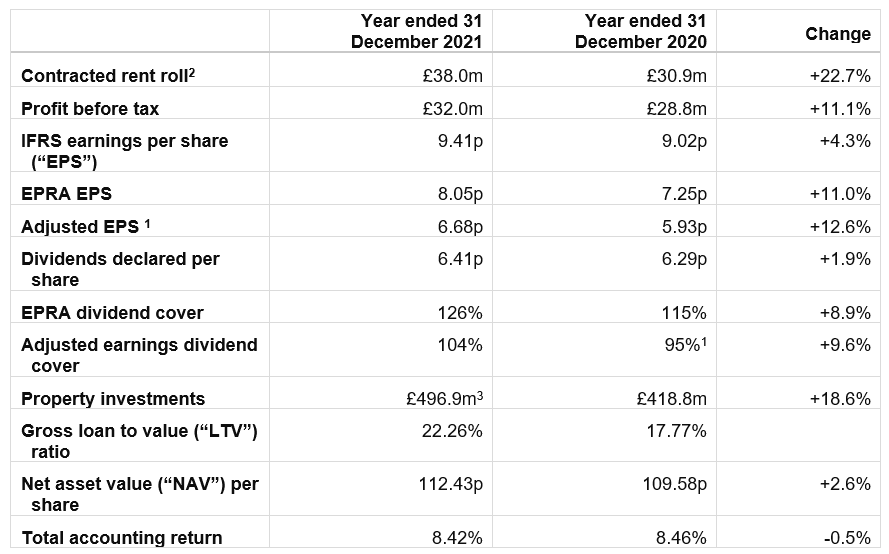

Financial highlights

- Contracted annual rent2 at 31 December 2021 was £38.0 million (2020: £30.9 million). 104 properties had rent reviews during the year, adding £0.7 million to the contracted rent, representing an annualised 2.5% increase on a like-for-like basis.

- Total accounting return comprised dividends paid in the year of 6.41p per share and NAV growth of 2.85p per share and totalled 8.42%, against our target of 9.0% per annum5.

- The Company has declared four quarterly dividends of 1.6025p each in respect of the year, meeting its target for 2021 of 6.41 pence per share.

- Dividends declared for the year were 126% covered by EPRA EPS and 104% covered by Adjusted EPS.

- Our dividend target for 2022 is 6.54p(5), representing 2.03% growth.

- EPS for the year was 9.41 pence (2020: 9.02 pence) and EPRA EPS was 8.05 pence (2020: 7.25 pence). Adjusted EPS, which better reflects underlying cash earnings in the year, was 6.68 pence (2020: 5.98 pence). All the EPS figures listed above are on both a basic and diluted basis.

- As at 31 December 2021, the portfolio was valued at £459.4 million, an increase of £40.6 million from the valuation of £418.8 million at 31 December 2020. The components of this valuation increase were as follows:

- acquisitions completed: £26.9 million;

- disposal: £1.3 million;

- acquisition costs capitalised: £1.3 million;

- capital improvements: £0.8 million; and

- valuation uplift: £12.9 million. Largely driven by rent increases received during the year.

- The NAV at 31 December 2021 was £394.2 million or 112.43 pence per share (31 December 2020: £349.5 million or 109.58 pence per share). NAV growth continued to be driven primarily by rental growth and the benefits of active asset management.

- This was an important year for the evolution of the Group’s debt financing, reflecting the growing maturity of the business. In the year we:

- Agreed a new £26 million NatWest facility, with an accordion agreement to extend up to £50 million.

- Secured the Group’s first long-term institutional fixed interest debt of £75 million facility with an average maturity 14 years. This provides an attractive fixed interest rate over the long term in an uncertain inflationary environment.

- The Group now has £168 million of available debt facilities, as well as the second £38 million tranche of institutional debt, which is committed to be issued in June 2022, and the option to expand the NatWest facility by a further £24 million.

Operational highlights

Against the backdrop of the ongoing COVID-19 pandemic, we have continued to deliver solid growth and attractive sustainable value to our stakeholders, demonstrating the resilience of both the Group, its portfolio and its tenants. Our tenants are established healthcare providers, offering good-quality care and earning fees from a broad spectrum of public sector customers and private-pay residents.

- Continued to collect 100% of rent due, with no changes to any lease terms or payment schedules.

- The portfolio remains 100% let.

- The Group continued to demonstrate its resilience throughout 2021 with rent cover rising to 1.95x (2020: 1.76x) including the benefit of grant funding.

- This is an important metric for both us and our tenants, as it reflects our tenants’ profitability and headroom against future cost pressures.

- At the year end the Group had investments in 124 properties with 6,720 beds.

- All leases are inflation-linked, with upwards-only rent reviews.

- EPRA ‘topped up’ net initial yield of 6.71% as at 31 December 2021 (31 December 2020: 6.71%). The average net initial yield of our acquisitions to date was 7.5%.

- Invested in 16 care homes for net consideration of £61.9 million, further diversifying the portfolio and adding 780 beds. 12 of these homes have been initially invested in through a loan of £37.5 million to allow the operator, Holmes Care Group, to acquire the assets with put and call options for us to acquire the assets for £1 once regulatory approvals are received.

- Committed to forward fund a property in Norwich with 80 beds, on a pre-let basis. The development site was purchased in the year for £2.4 million.

- The development we forward funded in Hartlepool is due to complete in 2022.

- Welcomed a new tenant, Carlton Hall, to the Group’s operators, giving us 134 tenants at the year end.

- The Group has grown its relationship with Holmes Care Group, contributing to the diversification of the tenant base and reducing exposure of contracted income from the Group’s main tenant, Minster Care Group, to 41% (2020: 48%).

- Weighted average unexpired lease term (“WAULT”) of 19.2 years at 31 December 2021 (31 December 2020: 20.0 years).

Sustainability – advancing our ESG agenda

- Completed EPC audit of the portfolio and assessed capital cost of improvements to achieve EPC band B.

- Commenced work on TCFD risk and opportunity analysis in preparation for full reporting.

- All new leases contain environmental obligations on tenants.

- Begun work on defining and measuring the social value of our investments.

Post-year end highlights

- Raised £40 million of gross proceeds from a placing of new ordinary shares.

- The Group completed the acquisition of two properties with 147 beds for £11.0 million in February 2022.

- The Group invested £11.1 million in two homes with 107 beds. The investment has initially been made by way of a loan to one of the Group’s existing tenants, Welford, to acquire the assets with put and call options for us to acquire the assets once regulatory approvals are received.

Notes

1 Adjusted earnings per share reflects underlying cash earnings per share in the period. The adjustments made to EPS in arriving at EPRA and Adjusted EPS are set out in note 10 to the Financial Statements. The inclusion of profit on disposal of investment property was made in the current year to better reflect the underlying cash earnings of the Group. The prior year adjusted earnings figure has been restated.

2 Contracted rent includes all post-tax income from investments in properties, whether generated from rental income or post-tax interest income.

3 This relates to the portfolio valuation along with loans to operators for the acquisition of property portfolios.

4 Including Croftwood and Minster, which are both part of the Minster Care Group.

5 This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

EPRA EPS and all other EPRA alternative performance measures have been calculated in line with EPRA best practices recommendation.

For the full RNS please see the attached document.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Mahesh Patel

Andrew Cowley

David Yaldron

Jefferies International Limited

Tom Yeadon tyeadon@jefferies.com

Neil Winward nwinward@jefferies.com

Francesco Namari fnamari@jefferies.com

Tel: +4420 7029 8000

Winterflood Securities Limited

Neil Langford neil.langford@winterflood.com

Joe Winkley joe.winkley@winterflood.com

Tel: +4420 3100 0000

Maitland/AMO (Communications Adviser)

James Benjamin impacthealth-maitland@maitland.co.uk

Alistair de Kare-silver

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

NOTES:

Impact Healthcare REIT plc acquires, renovates, extends and redevelops high quality healthcare real estate assets in the UK and lets these assets on long-term full repairing and insuring leases to high-quality established healthcare operators which offer good quality care, under leases which provide the Company with attractive levels of rent cover.

The Company aims to provide shareholders with an attractive sustainable return, principally in the form of quarterly income distributions and with the potential for capital and income growth, through exposure to a diversified and resilient portfolio of UK healthcare real estate assets, in particular care homes for the elderly.

The Company has a progressive dividend policy with a target to grow its annual aggregate dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year.

On this basis, the Company is targeting a dividend for the year to 31 December 2022 to increase by 2.0% to 6.54 pence per share*.

The Group’s Ordinary Shares were admitted to trading on the main market of the London Stock Exchange, premium segment, on 8 February 2019. The Company is a constituent of the FTSE EPRA/NAREIT index.

Neither the content of the Company’s website, nor the content on any website accessible from hyperlinks on its website for any other website, is incorporated into, or forms part of, this announcement nor, unless previously published by means of a recognised information service, should any such content be relied upon in reaching a decision as to whether or not to acquire, continue to hold, or dispose of, securities in the Company.

* This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

RESULTS PRESENTATION

A Company presentation for investors and analysts will take place at 08:30am (GMT) on the day via a live webcast and conference call.

To access the live webcast, please register in advance here:

https://www.lsegissuerservices.com/spark/ImpactHealthcareREIT/events/66e172be-4500-4633-9cf1-90cffbe35aa6

To access the live conference call, please contact Maitland/AMO at:

impacthealth-maitland@maitland.co.uk or by telephone on +44 (0) 20 7379 5151.

The recording of the webcast presentation and slides will be available later in the day via the Company website: https://www.impactreit.uk/investors/reporting-centre/presentations/