The board of Directors (the “Board“) of Impact Healthcare REIT plc (ticker: IHR), the real estate investment trust which gives investors exposure to a diversified portfolio of UK healthcare real estate assets, in particular care homes, is pleased to provide the following business and trading update for the quarter to 31 December 2021.

HIGHLIGHTS

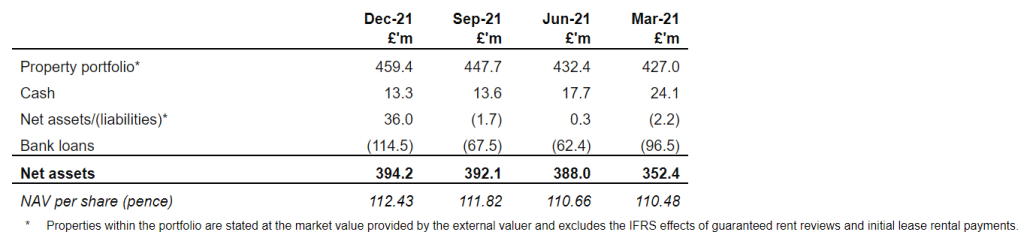

- Unaudited net asset value (“NAV“) as at 31 December 2021 of £394.2 million, 112.43 pence per share (NAV as at 30 September 2021: £392.1 million, 111.82 pence per share).

- The unaudited NAV total return for the quarter was 2.0%, comprising dividends paid in the quarter of 1.6025 pence and 0.61 pence per share growth in NAV.

- A dividend per ordinary share of 1.6025 pence declared today for the period, delivering on the Company’s annual dividend target of 6.41 pence per share for the year to 31 December 2021.

- The Company continues to deliver a covered dividend from both unaudited EPRA and unaudited Adjusted Earnings, with dividend cover of 127% and 107% from EPRA and Adjusted earnings respectively in the quarter, and 126% and 104% from EPRA and Adjusted earnings respectively for the year to 31 December 2021( 5).

- Holders of the New Ordinary Shares being issued pursuant to the Initial Issue, as set out below, will be eligible to receive this dividend in respect of the quarter ended 31 December 2021.

- As announced on 27 January 2022;

- The Company is targeting to raise gross proceeds of not less than £50 million through an initial issue of new Ordinary Shares of the Company (the “Initial Issue”) at 114.0 pence per New Ordinary Share (the “Issue Price”) by way of an Open Offer, Initial Placing, Offer for Subscription and Intermediaries Offer.

- The Company’s target dividend for the year to 31 December 2022 will increase by 2.0% to 6.54 pence per share (1), reflecting a 5.7% dividend yield on the Issue Price of 114.0 pence per New Ordinary Share.

- The Group’s property portfolio (“Portfolio“) was independently valued at £459.4 million as at 31 December 2021 (valuation as at 30 September 2021: £447.7 million). This represents a 0.4% increase in value on a like-for-like basis in the quarter, and a total increase of 2.6% over the quarter including an acquisition and a disposal.

- The like-for-like movements in value were primarily driven from RPI uplifts from rent reviews in the quarter.

- 13 rent reviews were completed in the quarter at an average uplift of 4% per annum in line with the rental increase cap on these leases.

- 100% of the Group’s rental income is linked to inflation, with 90.0% of the Group’s leases linked to RPI with a floor and cap at 2% p.a. and 4% p.a., 8.0% linked to RPI with a floor and cap at 1% p.a. and 5% p.a. and 2.0% with an annual CPI uplift.

- The portfolio EPRA ‘topped up’ Net Initial Yield at 31 December 2021 was 6.70% (30 September 2021 6.67%).

- The Group invested in 14 care homes in the quarter. 2 homes with 149 beds are reflected in the portfolio value outlined above. A further investment of £37.5 million in 12 homes with 480 beds was made initially by way of a loan to Holmes Care Group. Those homes will be included in the portfolio value upon Holmes Care exercising its option to repay the loan by delivering ownership of the 12 homes to Impact.

- The Group continues to receive 100% of rent payments as they fall due with no lease variations.

- Supporting the strong rent collection, rent cover in the fourth quarter of 2021 was 2.0 times across the Portfolio. This reflects the strong underlying growth of the average weekly fees, which the Group’s Tenants charge for the care they provide, along with a range of support measures introduced by the government to mitigate the pandemic including grant funding.

- The Group successfully secured £75.0 million in new long term institutional debt at a weighted average coupon of 2.967%, £37 million of which was drawn at the quarter end and a further £38 million will be drawn in June 2022. Gross loan to value ratio (“LTV“) was 22.3% as at 31 December 2021 (at 30 September 2021: 14.5%).

INITIAL ISSUE

- As announced on 27 January 2022, the Company is targeting to raise gross proceeds of not less than £50 million through an initial issue of new Ordinary Shares of the Company (the “Initial Issue”) at 114.0 pence per New Ordinary Share (the “Issue Price”) by way of an Open Offer, Initial Placing, Offer for Subscription and Intermediaries Offer.

- The Company will use proceeds from the Initial Issue to pay down its drawn revolving credit facilities, (currently £67.5 million). In addition, the Company’s investment manager, Impact Health Partners LLP (the “Investment Manager“) has £69 million of acquisitions in advanced legal discussions and a medium to longer term investment pipeline of over £290 million. The potential investment opportunities in the pipeline are managed by high-quality operators, are well maintained and offer the Company attractive levels of rent cover and a blended net initial yield in line with previous acquisitions made by the Company. In addition, the Company has committed to £26 million of forward funding and asset management capex, of which £16 million is yet to be deployed, and the Investment Manager has identified a longer-term asset management pipeline of a further 11 projects which would require a further £26 million of investment, which is anticipated to be accretive to both earnings and net asset value.

- The UK care home real estate market is supported by robust long term structural drivers and demographic fundamentals, including: increasing demand from a rapidly ageing population; an ongoing shortage of suitable supply that is fit for purpose; a need to reduce pressure on high-cost, medical care providers in the NHS; care operators with an established history of being able to pass inflationary pressures through fee increases; and the consolidation of a highly fragmented market. Meanwhile at an operational level, the Company’s tenants have over the past 12 months seen increasing occupancy rates, as the effect of the vaccination programme and the easing of pandemic restrictions feeds through, improving rental cover, with the potential for increased governmental funding over the longer term. The Company continues to benefit from these supportive trends, whilst its long-term inflation linked leases and conservative financial approach provides for additional potential value enhancement and downside protection.

NET ASSET VALUE

- Unaudited NAV as at 31 December 2021 of £394.2 million, 112.43 pence per share (unaudited NAV at 30 September 2021: £392.1 million, 111.82 pence per share).

- The unaudited NAV attributable to the ordinary shares of the Company is calculated under International Financial Reporting Standards (“IFRS“) and incorporates the independent portfolio valuation at 31 December 2021 and net income for the period. There is no difference between the IFRS NAV reported above and EPRA NTA.

- The unaudited NAV total return for the quarter was 2.0%, comprising dividends paid in the quarter of 1.6025 pence and 0.61 pence per share growth in NAV.

- Gross LTV of 22.3% as at 31 December 2021 (at 30 September 2021: 14.5%) following the draw down of the first phase of the Group’s new £75 million long term debt and a further £10 million under its existing revolving credit facilities. The Group has maintained a healthy level of cash reserves, which stood at £13.3 million at the quarter end.

Summary balance sheet (unaudited)

PROPERTY VALUATION

- The Group’s property portfolio (“Portfolio“) was independently valued at £459.4 million as at 31 December 2021 (valuation as at 30 September 2021: £447.7 million). This represents a 0.4% increase in value on a like for like basis in the quarter and a total increase of 2.6% over that period, including two acquisitions

- £1.6 million of this related to assets with rent reviews, a 3.4% increase in value on a like for like basis.

- £0.3 million was from yield movements due to underlying performance of the homes a 0.07% increase in value on a like for like basis.

- £9.5 million related to the acquisition of Hillcrest and Springhill and £0.2m on capital improvements.

- The portfolio EPRA ‘topped up’ Net Initial Yield at 30 September 2021 was 6.70% (30 September 2021: 6.67%).

- In addition to the £9.5m in acquisitions reflected in the portfolio value above, the group made an investment of £37.5 million in 12 homes with 480 beds by way of a loan to Holmes Care Group. Those homes will be included in the portfolio value upon Holmes Care exercising its option to repay the loan by delivering ownership of the 12 homes to Impact.

PORTFOLIO UPDATE

- The Group continues to receive 100% of rent payments as they fall due.

- Supporting the strong rent collection, rent cover in the fourth quarter of 2021 was 2.0 times across the Portfolio. This reflects the strong underlying growth of the average weekly fees, which the Group’s Tenants charge for the care they provide, along with a range of support measures introduced by the government to mitigate the pandemic including grant funding.

- Contracted rent increased to £38.0 million(2) at the quarter end (at 30 September 2021: £33.9 million) an increase of 12.1%. This increase was as a result of our investment in a portfolio of 12 homes with Holmes Group, the acquisition of Hillcrest and Springhill, and 13 rent reviews during the period.

- Portfolio changes in the quarter:

- The Group completed on the acquisition of a care home leased to Minster, with 88 registered beds in a small coastal town in the South West of England. The lease term is 20 years with upward-only Retail Price Index-linked rent reviews.

- Impact has completed the acquisition of Springhill Nursing care home in a sale and lease back with Silverline, one of the Group’s existing tenants. Springhill, located in Kilmarnock, Scotland, is a four storey Georgian building with a substantial purpose-built extension offering a total of 61 beds with en-suite wet room facilities. The lease term is 25 years with upward-only Retail Price Index-linked rent reviews.

- The Group has also invested in a portfolio of 12 care homes located in Fife, Scotland, offering 480 high quality en-suite beds, located within established residential areas. The investment has been made initially by way of a loan to Holmes Care Group which will allow it to complete the acquisition of Kingdom Homes immediately. The structure creates a number of benefits for all stakeholders, including enabling Holmes Care Group to take immediate operational control of the homes, thereby avoiding a potentially lengthy transition period, while regulatory approvals are sought to register the operation of the homes in new legal entities, as well as other financial and operational efficiencies.

- At 31 December 2021, the Portfolio comprised 126 healthcare properties(3), of which 124 are care homes let to 12 tenants (4) on fixed-term leases of 20 to 35 years (no break clauses). 100% of the Group’s rental income is linked to inflation, with 90.0% of the Group’s leases linked to RPI with a floor and cap at 2% p.a. and 4% p.a., 8.0% linked to RPI with a floor and cap at 1% p.a. and 5% p.a. and 2.0% with an annual CPI uplift.(6)

- Weighted average unexpired lease term across the Portfolio of 19.3 years as at 31 December 2021.

DIVIDEND DECLARATION AND 2022 DIVIDEND TARGET

- The Board has today declared the Company’s fourth interim dividend for the year ended 31 December 2021 of 1.6025 pence per ordinary share, payable on 11 March 2022 to shareholders on the register on 25 February 2022. The ex-dividend date will be 24 February 2022. This dividend will be paid as a Property Income Distribution (“PID”).

- This delivers Company’s annual dividend target of 6.41 pence per share for the year ended 31 December 2021.

- In line with the Company’s progressive dividend policy, under which it seeks to grow its target dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year, the target dividend for the year to 31 December 2022 will increase by 2.0% to 6.54 pence per share(1).

Notes:

(1) This is a target only and not a profit forecast. There can be no assurance that the target will be met and it should not be taken as an indicator of the Company’s expected or actual results.

(2) Contracted rent includes all post tax income from investment in properties, whether generated from rental income or post tax interest income.

(3) Includes exchanged and under construction assets.

(4) Minster and Croftwood (both subsidiaries of Minster Care Group), Careport, Prestige, Renaissance, Welford, Maria Mallaband Countrywide Group, NHS Cumbria, Optima, Holmes Care, Silverline, Electus Healthcare and Carlton Hall.

(5) Based on weighted average shares for the period. This does not take into consideration the incremental shares that will be issued as part of the proposed Initial Issue announced on 27 January 2022.

(6) Percentage allocation based on number of leases. Percentage allocation based on rental income is 88% subject to RPI uplifts of between 2% and 4%, 11% subject to RPI uplifts of between 1% and 5% and 1% are subject to CPI uplifts.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Impact Health Partners LLP via Maitland/AMO

Mahesh Patel

Andrew Cowley

David Yaldron

Jefferies International Limited

Tom Yeadon

Andrew Morris

Ollie Notts

Tel: +4420 7029 8000

Winterflood Securities Limited

Darren Willis

Neil Langford

Hande Derinkok

Tel: +4420 3100 0000

Maitland/AMO (Communications Adviser)

James Benjamin impacthealth-maitland@maitland.co.uk

Tel: +44 7747 113 930

The Company’s LEI is 213800AX3FHPMJL4IJ53.

Further information on Impact Healthcare REIT is available at www.impactreit.uk.

NOTES:

Impact Healthcare REIT plc acquires, renovates, extends and redevelops high quality healthcare real estate assets in the UK and lets these assets on long-term full repairing and insuring leases to high-quality established healthcare operators which offer good quality care, under leases which provide the Company with attractive levels of rent cover.

The Company aims to provide shareholders with an attractive sustainable return, principally in the form of quarterly income distributions and with the potential for capital and income growth, through exposure to a diversified and resilient portfolio of UK healthcare real estate assets, in particular care homes for the elderly.

The Company has a progressive dividend policy with a target to grow its annual aggregate dividend in line with the inflation-linked rental uplifts received by the Group under the terms of the rent review provisions contained in the Group’s leases in the prior financial year.

On this basis, the target total dividend for the year ending 31 December 2022 is 6.54 pence per share1, a 2.0% increase over the 6.41 pence in dividends paid or declared per ordinary share for the year ended 31 December 2021.

The Group’s Ordinary Shares were admitted to trading on the main market of the London Stock Exchange, premium segment, on 8 February 2019. The Company is a constituent of the FTSE EPRA/NAREIT index.